Blockchain is a decentralized and distributed digital ledger technology used to securely and tamper-proof record transactions across many computers. It was designed to support the digital currency Bitcoin, but it has since been adapted for use in finance, supply chain management, and healthcare.

A blockchain is a database maintained by a network of computers or nodes, each with a copy of the ledger. Transactions are validated and added to the catalog via a process known as consensus, in which most nodes agree that the transaction is valid.

One of the most important aspects of blockchain is its security. Because each block in the chain is linked to the previous block via a cryptographic hash, an attacker would have difficulty altering the data in the ledger without being detected. This makes blockchain helpful for applications requiring secure and transparent record-keeping.

Blockchain technology can eliminate the need for intermediaries in certain transactions, such as financial transfers and real estate transactions. Lowering costs, shortening processing times, and increasing transparency and accountability are all possible outcomes.

Importance of Blockchain

Blockchain is essential for several reasons:

Decentralization

One of the most important characteristics of blockchain is its decentralization, which means it is not controlled by a centralized authority but rather by a network of nodes. Because there is no single point of failure, it is resistant to censorship and manipulation.

Security

Blockchain employs cryptographic algorithms to secure the data stored on the network. This makes it extremely difficult for hackers to manipulate data without being detected. This makes it suitable for secure and tamper-resistant record-keeping applications, such as financial transactions and supply chain management.

Transparency

All network nodes can access the same data because blockchain is a distributed ledger, enabling the development of transparent, open, and auditable systems.

Efficiency

Many processes that require manual intervention, such as financial transaction clearing and settlement, can be automated using blockchain. This can result in faster and more efficient operations and lower costs.

Trust

Blockchain can help to build trust between strangers by providing a secure and transparent record of transactions. This is especially useful when trust is essential, such as in financial transactions or supply chain management.

Critical Elements of Blockchain

The essential elements of a blockchain are:

Distributed Ledger

A blockchain is a distributed digital ledger shared by a network of computer nodes, and this ledger contains a record of all transactions on the internet.

Blocks

Transactions are grouped into blocks, which are added to the blockchain in chronological and linear order. Each block in the chain contains a reference to the block before it, resulting in a chain of blocks that cannot be changed without affecting the entire chain.

Consensus

To add a block to the blockchain, most nodes on the network must agree that the transaction is valid. This consensus mechanism ensures the blockchain’s integrity and security.

Cryptography

Blockchain employs cryptography to secure the network’s transactions and blocks. Transactions are signed with a private key, which anyone with the corresponding public key can verify. Cryptographic hashes are used to secure blocks, making it difficult for attackers to tamper with the data in the block.

Smart Contracts

A smart contract is self-executing and stored on the blockchain. Smart contracts can automate the execution of complex agreements such as financial transactions and supply chain management.

Decentralization

Blockchain is a decentralized system, meaning any central authority does not control it. It is instead maintained by a network of nodes, each of which has a copy of the ledger. As a result, it is resistant to censorship and manipulation.

How Blockchain Works?

Blockchain creates a decentralized and distributed ledger that securely and tamper-proof records transactions between two parties.

You can find out more about blockchain by visiting Simplilearn.

Here’s a quick rundown of how blockchain works:

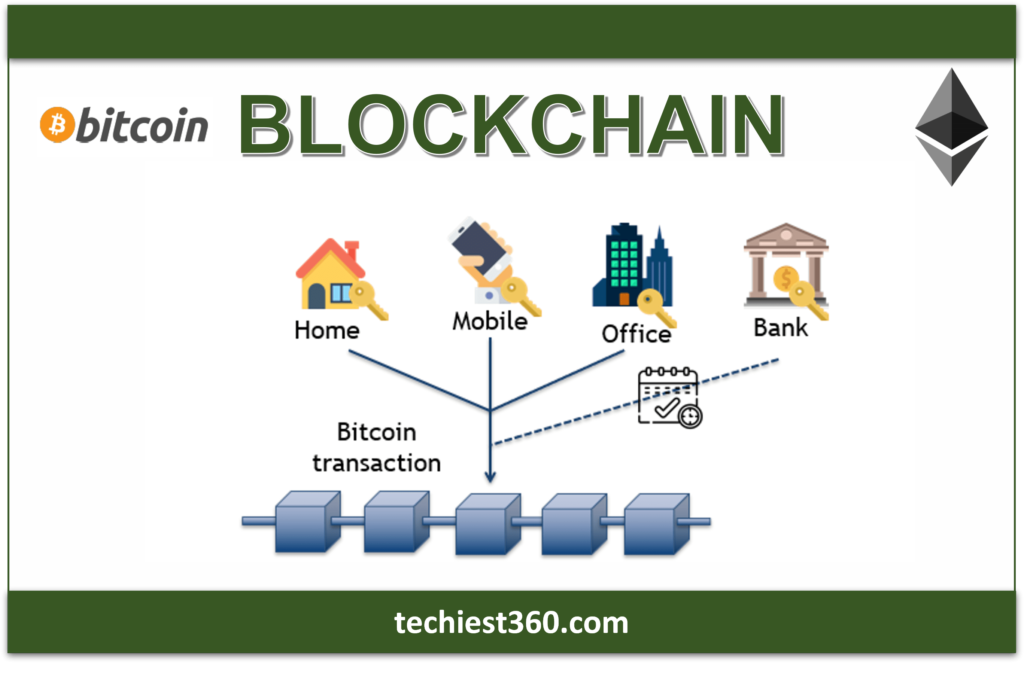

Transactions

On the blockchain, a transaction is initiated between two parties. This transaction can involve exchanging anything of value, such as money, data, or even physical goods.

Verification

A blockchain network of nodes verifies the transaction. Each network node has a copy of the ledger and validates the transaction by ensuring the sender has sufficient funds or authorization to carry out the transaction.

Block Creation

Once verified, the transaction is combined with other transactions to form a block. Each block contains a unique cryptographic hash that connects it to the previous block in the blockchain, creating an immutable chain of blocks.

Consensus

Before a block can be added to the blockchain, most network nodes must agree that the transaction is valid. This consensus mechanism ensures the blockchain’s integrity and security.

Block Addition

After reaching a consensus, the block is added to the blockchain and becomes a permanent ledger. This block is then distributed to all network nodes, ensuring each node has an accurate and up-to-date copy of the ledger.

Mining

Nodes in some blockchain systems can be rewarded for adding blocks. Mining is adding a block to the chain by solving complex mathematical problems.

Benefits of Blockchain

Blockchain has several advantages, including:

Decentralization

Blockchain is a decentralized system, which means a centralized authority does not govern it. It is instead kept up by a network of nodes, each of which has a copy of the ledger. As a result, it is resistant to censorship and manipulation.

Security

Blockchain employs cryptography to secure the network’s transactions and blocks. Transactions are signed with a private key, which anyone with the corresponding public key can verify. Cryptographic hashes are used to secure blocks, making it difficult for attackers to tamper with the data in the block.

Transparency

All network nodes can access the same data because blockchain is a distributed ledger, enabling the development of transparent, open, and auditable systems.

Efficiency

Many processes that currently require manual intervention, such as financial transaction clearing and settlement, can be automated by blockchain. This can result in faster and more efficient operations and lower costs.

Trust

Blockchain can help to build trust between strangers by providing a secure and transparent record of transactions. This is especially useful in situations requiring trusts, such as financial transactions or supply chain management.

Immutable record-keeping

Once added to the blockchain, a transaction cannot be changed without affecting the entire chain. This results in a tamper-proof, permanent record of transactions that can be relied on.

Interoperability

Blockchain can aid in developing interoperable systems that allow different organizations to collaborate seamlessly. This may result in increased collaboration and innovation across industries and sectors.

Types of Blockchain Networks

There are three main types of blockchain networks:

Public Blockchain

A public blockchain is a decentralized network that anyone interested can access. This network is commonly used for cryptocurrencies, and anyone can create a wallet and join the network. On public blockchains, transactions are validated using a consensus mechanism such as proof-of-work or proof-of-stake.

Private Blockchain

A private blockchain is a network with limited participants, and this network type is frequently used in enterprise settings where the participants are known and trusted. Because they do not require as much computational power to validate transactions, private blockchains can be faster and more efficient than public blockchains.

Consortium Blockchain

A consortium blockchain is a business-owned and operated network. This type of network is frequently used for collaborative projects in which participants must securely and transparently share information and data. Depending on the needs of the participants, consortium blockchains can be either public or private.

Blockchain Security

Several security features built into blockchain technology make it difficult for attackers to manipulate data on the network.

To secure data on the network, blockchain employs cryptographic techniques. A private key is used to sign transactions, and a public key is used to verify them. Cryptographic hashes secure blocks, making it difficult for attackers to modify data in a block without being detected.

No single control point exists because blockchain is a decentralized system. Instead, the data is stored on a distributed ledger, with copies kept by all network nodes. This makes it difficult for attackers to manipulate network data because they must compromise most nodes.

Blockchain employs consensus mechanisms such as proof-of-work or proof-of-stake to validate transactions and add new blocks to the chain. This ensures that all network nodes agree on the ledger’s state and that most nodes approve any changes.

Once a transaction has been added to the blockchain, it cannot be changed or removed without affecting the entire chain. This results in a tamper-proof, permanent record of transactions that can be relied on.

On the blockchain, smart contracts are self-executing programs. They can be used to automate processes and enforce rules, making it easier to ensure the security and validity of network transactions. While blockchain provides several security features, it is critical to be aware of potential vulnerabilities such as code bugs, attacks on individual nodes, and social engineering attacks. As with any technology, it is essential to follow security best practices, such as using strong passwords, keeping software up to date, and exercising caution when sharing sensitive information.

Blockchain Use Cases and Applications

Blockchain is a distributed ledger technology that enables secure and transparent data storage. Here are some blockchain use cases and applications:

Cryptocurrencies

Blockchain technology is best known for its application in cryptocurrencies such as Bitcoin and Ethereum. These digital currencies employ blockchain technology to securely record transactions and provide a decentralized method of transferring value without intermediaries such as banks.

Supply Chain Management

Blockchain technology can track goods and products moving through the supply chain. This can help increase transparency while lowering the risk of fraud and counterfeiting.

Identity Management

Blockchain can securely store and manage digital identities, allowing for a decentralized and tamper-proof method of identity verification.

Voting Systems

Blockchain technology can create secure and transparent voting systems resistant to fraud and manipulation.

Smart Contracts

Blockchain technology can create self-executing contracts that are automatically enforced when certain conditions are met. This can aid in the streamlining of business processes and the elimination of the need for intermediaries.

Healthcare

Blockchain technology can securely store and share medical data, allowing for more efficient and secure patient record management.

Real Estate

Blockchain technology can be used to securely and transparently record property transactions, improving efficiency and lowering the risk of fraud.

Energy Management

By enabling peer-to-peer energy trading and more efficient energy production and consumption management, blockchain can help manage energy grids and reduce energy waste.

Blockchain Protocols

Blockchain protocols are the rules and algorithms that govern how a blockchain network operates. Several blockchain protocols are used today, each with features and characteristics. The following are some of the most widely used blockchain protocols:

Bitcoin

The first and most well-known blockchain protocol is Bitcoin, and it is based on a proof-of-work consensus algorithm and records transactions using a public ledger.

Ethereum

Ethereum is a blockchain protocol that allows smart contracts and decentralized applications to be created. It uses a public ledger to record transactions based on a proof-of-stake consensus algorithm.

Ripple

Ripple is a blockchain protocol designed for international payments and settlement. It employs the Ripple Protocol Consensus Algorithm (RPCA) and a private ledger to record transactions.

Hyperledger

Hyperledger is an open-source blockchain protocol for enterprise applications. It can create private or permissioned blockchains and employs several consensus algorithms, including proof-of-stake and practical Byzantine fault tolerance (PBFT).

Corda

Corda is a blockchain protocol intended for financial applications. It employs a consensus algorithm known as notary consensus and a private ledger to record transactions.

EOS

EOS is a blockchain protocol built for fast transactions and decentralized applications. It employs a delegated proof-of-stake consensus algorithm and a public ledger to record transactions.

You can find more posts related to technology by clicking here.